Table of Contents

T E C H C H O R A GLOBAL FINANCIAL TECHNOLOGY RESEARCH & ANALYSIS

RESEARCH REPORT | INFRASTRUCTURE & PAYMENTS

An authoritative examination of the structural evolution of international settlement systems, the concept of financial fungibility, and the growing role of regulated fintech infrastructure companies in enabling real-time global liquidity movement.

Publication: TechChora Infrastructure & Payments April 2026

The global cross-border payments market, valued at approximately $190 trillion in annual transaction volume, remains one of the most structurally inefficient segments of the international financial system. Despite decades of incremental reform, the fundamental architecture of international money movement, built atop correspondent banking networks established in the post-Bretton Woods era, continues to impose material friction costs on the global economy. The World Bank estimates that the average cost of sending $200 internationally remains above 6%, nearly three times the UN Sustainable Development Goal target of 3%, while settlement times in many corridors still extend across two to five business days.

Into this structural gap has entered a new class of financial infrastructure companies. These are not consumer-facing fintech applications competing on user experience, but foundational settlement and treasury infrastructure providers building the rails upon which global money movement will increasingly depend. They operate at the technical and regulatory intersection of traditional correspondent banking, real-time payment networks, and digital asset settlement systems.

Swetche Systems Limited, founded by Lucky Koiza Oyanna and operating across Estonia, Canada, the United Kingdom, and Nigeria, represents an instructive case study in this infrastructure-first approach. With settlement reach spanning 150-plus countries, support for more than 41 currencies, and a regulatory architecture encompassing International Money Transfer Operator (IMTO) licensing across two jurisdictions, Money Services Business (MSB) registration, and Bureau de Change compliance frameworks, Swetche has positioned itself as a multi-jurisdictional treasury and cross-border settlement infrastructure provider serving institutions, exporters, and payment processors rather than retail consumers.

This analysis examines the systemic forces driving the evolution of cross-border payments infrastructure, the emerging concept of financial fungibility as an organizing framework for next-generation settlement systems, and the strategic implications of infrastructure-led fintech companies for global trade, financial inclusion, and the competitive dynamics of international finance.

| $190T

Global cross-border payment volume annually |

6%+

Average cost to send $200 internationally |

150+

Countries in Swetche’s settlement network |

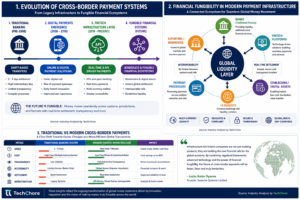

The Global Cross-Border Payments Challenge

The inefficiency of cross-border payments is not a peripheral concern of the international financial system. It is one of its defining structural constraints. For businesses engaged in global trade, exporters in emerging markets, migrant workers remitting earnings to home countries, and financial institutions managing multi-currency treasury operations, the cost and latency of international money movement represent real, quantifiable drags on economic output.

The correspondent banking model, which has governed international payments for over a century, operates through chains of bilateral relationships between banks. When a company in Lagos wishes to pay a supplier in Hamburg, the transaction typically traverses a chain of correspondent relationships, often involving three to five intermediary institutions, each of which extracts a fee, applies a proprietary foreign exchange spread, and introduces processing delays. The resulting transaction, which in principle represents a simple transfer of economic value between two counterparties, may take three business days, cost between 3% and 8% of the principal amount, and offer the sender limited visibility into its real-time status.

This friction is not merely inconvenient. It is economically consequential. The McKinsey Global Institute has estimated that reducing the cost of cross-border payments to near-zero levels would add hundreds of billions of dollars to global GDP annually, primarily by enabling transactions that are currently economically unviable at prevailing cost structures. For small and medium enterprises in developing economies, the friction of international payments represents a structural competitive disadvantage relative to counterparts in markets with more efficient financial infrastructure.

According to recent global financial reporting by Reuters, cross-border payment inefficiencies remain a major constraint to international trade, particularly in emerging markets where settlement delays and foreign exchange volatility continue to impact business operations.

The COVID-19 pandemic accelerated awareness of this fragility. Supply chain disruptions revealed how dependent global trade is on the smooth, rapid movement of payments, and how the failure of even one link in the correspondent banking chain could freeze liquidity for thousands of downstream counterparties. This systemic vulnerability has intensified regulatory and private sector interest in alternative settlement architectures: real-time payment networks, ISO 20022 migration, central bank digital currencies (CBDCs), and stablecoin-based settlement systems.

The Rise of Infrastructure-Led Fintech

The history of international payment infrastructure is, in essence, a history of successive attempts to reduce the friction inherent in moving value across jurisdictional boundaries. SWIFT, the Society for Worldwide Interbank Financial Telecommunication, was established in 1973 precisely to bring standardization and efficiency to the manual, paper-intensive correspondent banking processes of its era. For several decades, SWIFT represented the gold standard of international payments coordination, enabling banks across 200 countries to exchange standardized financial messages with a degree of reliability and security previously unachievable.

However, SWIFT was designed as a messaging network, not a settlement network. It communicates payment instructions; the actual movement of funds still depends on bilateral correspondent relationships and the liquidity pools that banks maintain in nostro and vostro accounts around the world. This architectural constraint, the separation of messaging from settlement, is the root source of much of the latency and cost embedded in international payments today.

The subsequent evolution of payment infrastructure has proceeded along several parallel tracks. Within individual markets, real-time payment networks have emerged to enable near-instantaneous domestic transfers. The UK’s Faster Payments Service, India’s Unified Payments Interface (UPI), Brazil’s Pix system, and the United States’ FedNow service represent the current state of the art in domestic real-time settlement. These systems have demonstrated unambiguously that instantaneous, low-cost settlement is technically achievable. The challenge lies in extending this capability across jurisdictional boundaries.

Perhaps most significantly, the emergence of digital asset networks, initially in the form of public blockchains and more recently as regulated stablecoin infrastructure, has introduced a genuinely novel settlement architecture. In this model, value can be transferred between jurisdictions without traversing a correspondent banking chain, with settlement finality achieved in seconds rather than days.

“A truly fungible international payment system would enable a naira balance held by a Nigerian exporter to be converted, transferred, and received as euros by a European counterparty in real time, at minimal cost, with full regulatory compliance, and with the same certainty as a domestic transfer.”

Understanding Financial Fungibility

Financial fungibility refers to the capacity of money to move seamlessly across systems, jurisdictions, formats, and rails without friction, loss of value, or degradation of utility. It has emerged as a central organizing concept for next-generation payment infrastructure. While fungibility has always been a theoretical property of money, its practical realization in cross-border contexts has historically been limited by structural constraints.

The concept of financial fungibility encompasses several distinct dimensions. Asset fungibility refers to the interchangeability of different monetary instruments, including fiat currencies, stablecoins, and central bank digital currencies, within a unified settlement architecture. Rail fungibility refers to the ability of a payment to traverse multiple settlement networks, from SWIFT to local real-time payment networks and blockchain-based rails, with seamless handoffs and consistent settlement finality. Jurisdictional fungibility refers to the capacity of a payment infrastructure to operate within compliance frameworks across multiple sovereign regulatory environments simultaneously.

For infrastructure providers like Swetche Systems Limited, achieving meaningful fungibility across all three dimensions is the defining technical and regulatory challenge. The company’s support for 41-plus currencies and settlement reach across 150-plus countries reflects an aspiration toward asset and jurisdictional fungibility. Its integration of both fiat and regulated stablecoin settlement rails reflects an approach to rail fungibility that acknowledges the coexistence, rather than the replacement, of traditional and digital settlement architectures.

Recent coverage on TechCrunch highlights the rapid rise of infrastructure-led fintech companies building scalable solutions for cross-border payments, treasury management, and global financial interoperability.

The economic significance of enhanced fungibility extends well beyond payments efficiency. When money becomes more fungible and can move across borders with the same ease that it moves within them, the effective integration of global capital markets deepens. Exporters in emerging markets gain access to working capital at lower cost. Importers can manage currency risk more effectively. Multinational corporations can optimize their global treasury operations with greater precision. And workers in diaspora communities can transfer earnings to families in home countries without surrendering a disproportionate fraction to intermediary costs.

Case Study: Swetche Systems Limited

| COMPANY PROFILE

Swetche Systems Limited | Founded by Lucky Koiza Oyanna Operations: Estonia, Canada, United Kingdom, Nigeria IMTO Licenses: Nigeria & Canada | MSB Registration: Canada | Bureau de Change Compliance Settlement reach: 150+ countries | 41+ currencies | Fiat & regulated stablecoin rails |

Swetche Systems Limited occupies a distinctive position in the global cross-border payments landscape. Founded by Lucky Koiza Oyanna, a finance professional whose career has spanned funds transfer operations at Sterling Bank Plc, financial management at an institutional library foundation, and procurement and treasury systems development, Swetche has been structured from inception as an infrastructure provider rather than a consumer-facing payments application.

This positioning is strategically significant. The consumer-facing segment of the payments market, dominated by companies such as Wise, Remitly, and WorldRemit, is characterized by intense competition, thin margins, and regulatory complexity driven by consumer protection requirements. The infrastructure segment, by contrast, serves institutional clients including banks, payment processors, exporters, and treasury management operations, with higher transaction volumes, more predictable revenue, and a differentiated regulatory profile.

Swetche’s operational geography, spanning Estonia, Canada, the United Kingdom, and Nigeria, is not arbitrary. Each jurisdiction represents a strategic node in the company’s global settlement network. Estonia, as an EU member state, provides access to the European payments infrastructure and the EU regulatory passport. Canada, with its MSB registration framework and IMTO licensing, provides access to North American dollar flows and the substantial Canadian diaspora remittance corridors. The United Kingdom, with its robust MSB regulatory framework and position as the world’s leading international financial center, provides access to sterling liquidity and global institutional counterparties. Nigeria, with its IMTO licensing, positions Swetche at the center of Africa’s largest economy and most significant remittance destination.

The company’s regulatory architecture is particularly noteworthy. Holding IMTO licenses in both Nigeria and Canada simultaneously is a non-trivial regulatory achievement. The Central Bank of Nigeria’s IMTO framework imposes stringent capital requirements, operational standards, and reporting obligations on licensed operators. Meeting these requirements while simultaneously maintaining MSB compliance in Canada and operating within Bureau de Change frameworks for cash-based transactions requires sophisticated compliance infrastructure and genuine regulatory expertise.

Swetche’s workforce of approximately 30 professionals, some of whom are remunerated in foreign currency, is itself a demonstration of the company’s operational model. A payroll denominated partially in foreign currencies reflects not merely an international operational footprint but an active deployment of the cross-currency treasury capabilities that the company offers to its clients. A company that lives within the problem it is solving develops operational insights that purely transactional infrastructure providers cannot replicate.

The company’s founder has also positioned Swetche within a broader advocacy context, earning recognition from the International Association of World Peace Advocates (IAWPA) and the United Nations Peace Volunteers Chartered Fellowship for IMTO. This positioning reflects an understanding that cross-border payment infrastructure is not merely a technical or commercial question but a dimension of international economic integration with direct implications for development, stability, and the quality of bilateral economic relationships.

| 41+

Currencies supported across settlement network |

$50B

Annual remittances received by sub-Saharan Africa |

7.8%

Average remittance cost to sub-Saharan Africa |

How Modern Payment Systems Are Evolving

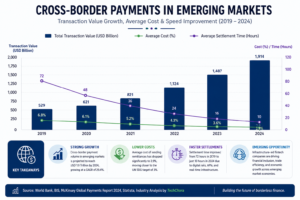

No region of the world is more acutely affected by the inefficiencies of cross-border payments than sub-Saharan Africa. The continent receives approximately $50 billion in remittances annually, making it one of the world’s largest remittance destinations in absolute terms and, as a percentage of GDP for many individual countries, the most remittance-dependent. Yet Africa consistently records the highest average remittance costs globally. The World Bank’s Remittance Prices Worldwide database estimates that the average cost of sending $200 to sub-Saharan Africa exceeds 7.8%, well above the global average and the SDG 10.c target of 3%.

These costs are driven by a combination of structural and regulatory factors. The limited penetration of formal banking infrastructure in many African markets reduces the addressable market for digital remittance products, maintaining the dominance of cash-based transfer mechanisms with inherently higher unit costs. The fragmentation of African payment systems across 54 sovereign regulatory jurisdictions creates compliance complexity that deters international payment providers from investing in corridor infrastructure. The limited availability of dollar and euro liquidity in local banking systems also creates FX premiums that inflate the effective cost of currency conversion.

Nigeria represents a particularly instructive case. As Africa’s largest economy and most populous nation, Nigeria receives remittance flows estimated at $20 billion annually, making it the largest single remittance destination on the continent. The country’s dual exchange rate environment, now substantially reformed although historical distortions persist, its history of currency controls, and the complexity of its banking regulatory environment have created significant barriers to efficient international money movement. At the same time, Nigeria’s large and economically active diaspora communities in the United Kingdom, United States, and Canada create deep demand for improved remittance infrastructure.

The CBN’s IMTO licensing framework represents a regulatory effort to channel international money flows through regulated, accountable operators while developing the domestic infrastructure necessary to support efficient settlement. For a company like Swetche, operating with IMTO licensing in Nigeria, this regulatory framework is both a compliance burden and a competitive moat. It is a barrier to entry that, once cleared, provides access to one of the world’s most significant remittance corridors.

Beyond remittances, the cross-border payment challenge in Africa directly affects international trade. African exporters, particularly in agricultural commodities, manufactured goods, and professional services, face disproportionate friction in receiving payments from international buyers. Swetche’s explicit focus on equipping exporters with the financial infrastructure and knowledge to compete effectively in global markets reflects a concrete understanding of this broader economic context.

The Role of Stablecoins in Global Liquidity

The integration of stablecoin settlement rails into cross-border payment infrastructure represents perhaps the most consequential architectural development in international payments since the establishment of SWIFT. Stablecoins are digital assets designed to maintain a stable value relative to a reference currency or basket of currencies. They have demonstrated a genuinely novel capacity to enable near-instantaneous, low-cost settlement across jurisdictional boundaries without the intermediation of a correspondent banking chain.

The dollar-denominated stablecoin market, led by USDT (Tether) and USDC (Circle), had reached a combined circulating supply of over $200 billion as of early 2026, representing a substantial and growing pool of dollar liquidity accessible through blockchain-based settlement rails. For cross-border payment providers, stablecoins offer several distinct advantages over traditional settlement architectures. Settlement finality can be achieved in seconds rather than days. Transaction costs are denominated in network fees rather than intermediary spread. Geographic reach is effectively unlimited by the public accessibility of blockchain networks. And the programmability of smart contract-based settlement enables sophisticated automated treasury management functions that are difficult to replicate in traditional banking infrastructure.

As explored in a broader technology analysis by Wired, the convergence of traditional finance and digital asset infrastructure is accelerating the development of more efficient and programmable global payment systems.

However, the integration of stablecoin rails into regulated payment infrastructure introduces a set of compliance and operational challenges that require careful management. The regulatory classification of stablecoins varies considerably across jurisdictions, from relatively permissive frameworks in Singapore, Switzerland, and the UAE to more restrictive approaches in certain G7 markets. Cross-border payment providers seeking to integrate stablecoin settlement must navigate this regulatory fragmentation, ensuring that their use of digital assets is compliant with the requirements of every jurisdiction in which they operate.

For Swetche Systems Limited, the integration of regulated stablecoin rails alongside traditional fiat settlement infrastructure represents a practical implementation of the rail fungibility concept. By maintaining the capability to route payments through either traditional correspondent banking networks or stablecoin-based rails, selecting the most efficient path for a given corridor and transaction size, the company can optimize for cost, speed, and regulatory compliance simultaneously.

The longer-term implications of stablecoin adoption in cross-border settlements extend beyond individual payment efficiency. As stablecoin liquidity deepens, the FX premium embedded in cross-currency transactions in less-liquid corridors, a significant cost driver for payments involving African, South Asian, and Latin American currencies, should compress. The existence of a reliable, low-cost dollar settlement layer creates gravitational pull toward dollar-denominated financial intermediation with significant implications for monetary sovereignty in emerging market economies.

Regulatory Environment and Compliance Systems

The regulatory landscape for cross-border payments is among the most complex in financial services, characterized by overlapping national frameworks, evolving international standards, and the fundamental tension between financial inclusion objectives and anti-money laundering (AML) and counter-terrorism financing (CTF) requirements.

The global trend toward correspondent banking de-risking, namely the withdrawal of major banks from correspondent relationships with institutions in higher-risk jurisdictions, has created a significant gap in formal financial infrastructure precisely where it is most needed. The IMF and World Bank have documented the decline in correspondent banking relationships as a macro-financial risk, noting that it forces financial flows into informal channels that are more opaque and harder to monitor than the regulated banking system.

IMTO licensing frameworks, such as those operated by the Central Bank of Nigeria and equivalent authorities in Canada, represent a regulatory architecture specifically designed to address this gap. By creating a licensed category of non-bank financial institution authorized to conduct international money transfers, these frameworks enable regulated, compliant cross-border payment operations outside the traditional correspondent banking system.

For a multi-jurisdictional infrastructure provider like Swetche, maintaining compliance across multiple regulatory frameworks simultaneously is a significant operational investment. Canada’s MSB registration under FINTRAC imposes AML/CTF compliance obligations consistent with FATF standards. The UK’s MSB framework under the Financial Conduct Authority (FCA) imposes similar requirements with additional provisions related to consumer protection and operational resilience. Nigeria’s IMTO framework adds currency-specific reporting requirements and capital controls compliance. The Bureau de Change framework introduces physical compliance requirements related to cash handling and documentation.

The cumulative compliance burden of maintaining good standing across these frameworks is substantial, and deliberately so. Regulatory legitimacy is, in the payment infrastructure business, not a constraint on value creation but a genuine source of it. Institutional clients including banks, payment processors, and corporate treasury operations will only entrust cross-border settlement to partners whose regulatory standing is beyond question.

“Regulatory legitimacy is, in the payment infrastructure business, not a constraint on value creation but a genuine source of it. Institutional clients will only entrust cross-border settlement to partners whose regulatory standing is beyond question.”

Global Comparative Analysis

The evolution of cross-border payment infrastructure is occurring simultaneously across multiple geographies, each with distinctive structural characteristics, regulatory environments, and pace of development. A comparative analysis of major regional payment ecosystems illuminates both the diversity of approaches to this challenge and the convergent pressures driving infrastructure innovation globally.

In Africa, the fintech ecosystem has developed rapidly but unevenly. East Africa, led by Kenya’s M-Pesa mobile money infrastructure, has achieved high levels of digital financial inclusion within domestic markets, but cross-border connectivity between African payment systems remains limited. The Pan-African Payment and Settlement System (PAPSS), launched by the African Export-Import Bank in 2022, represents the most ambitious attempt to date to create a unified intra-African payment infrastructure, enabling transactions between African countries in local currencies without dollar intermediation.

In Europe, the Single Euro Payments Area (SEPA) has effectively solved the domestic cross-border payment problem within the eurozone, enabling instant euro transfers between any of the 36 participating countries at near-zero marginal cost. SEPA’s success, achieved through regulatory harmonization, technical standardization, and the political commitment of EU member states, provides a template for regional payment integration that is increasingly studied in other parts of the world. The EU’s MiCA frameworks extend this harmonization to digital asset settlement, creating a coherent regulatory environment for stablecoin operations.

In North America, the United States’ FedNow service, launched in 2023, represents a significant step toward real-time domestic settlement. Canada’s Payments Modernization initiative, which includes the implementation of ISO 20022 messaging standards and the Real-Time Rail (RTR), is advancing on a broadly similar trajectory. For remittance corridors connecting North America with Latin America, Africa, and Asia, collectively among the world’s highest-volume payment flows, the modernization of US and Canadian domestic infrastructure creates the upstream conditions for more efficient cross-border settlement.

In Asia, India’s UPI system has achieved extraordinary scale, processing over 100 billion transactions annually, and has begun to extend its reach through bilateral connectivity agreements with Singapore, the UAE, and several other markets. Singapore has positioned itself as a global hub for payment infrastructure innovation, with the Monetary Authority of Singapore’s Project Ubin and subsequent initiatives exploring blockchain-based settlement for international payments.

The Role of Infrastructure Fintech Companies

The emergence of infrastructure-focused fintech companies represents a structural evolution in the financial services industry that deserves analytical attention distinct from the consumer fintech phenomenon. While consumer fintech companies such as Revolut, Nubank, and N26 have attracted enormous capital by competing with retail banks on user experience, the more consequential transformation of global financial infrastructure is being driven by companies that serve institutions rather than individuals.

Infrastructure fintech companies function as financial system middleware, the invisible plumbing that enables value to move between user-facing applications and the fundamental settlement layer of the financial system. They are to the payments economy what cloud computing providers are to the digital economy: invisible to end users, essential to the functioning of the system, and increasingly concentrated in the hands of specialized operators with the technical and regulatory expertise to operate at scale.

Industry commentary from The Verge also points to a growing shift toward backend financial infrastructure, where fintech companies are focusing less on consumer apps and more on powering the systems that enable seamless global transactions.

This infrastructure layer encompasses several distinct functional categories. Settlement infrastructure providers, the category in which Swetche operates, specialize in the actual movement of value between jurisdictions, managing the FX conversion, liquidity provision, and regulatory compliance functions that cross-border settlement requires. Treasury management infrastructure providers offer tools and systems including multi-currency accounts, FX hedging instruments, and cash pooling mechanisms that enable multinational corporations and financial institutions to optimize their global liquidity positions.

The value proposition of infrastructure-focused fintech companies relative to traditional banks is fundamentally one of specialization. The correspondent banking system requires major banks to maintain relationships and liquidity pools in hundreds of markets simultaneously, a scale-intensive, capital-intensive operation that is inherently difficult to optimize for the unique requirements of any particular payment corridor. Specialized infrastructure providers can focus their capital and regulatory investment on specific corridors, currency pairs, and client types, achieving levels of efficiency and service quality that generalist banks cannot match.

Founder: Lucky Koiza Oyanna’s Vision

The evolution of a financial infrastructure company from concept to regulated, multi-jurisdictional operation requires a founder whose background provides genuine insight into the structural problems being addressed. Lucky Koiza Oyanna’s professional trajectory, from funds transfer operations at Sterling Bank Plc where he developed hands-on understanding of the mechanics of international money movement, through financial management roles and ultimately to the founding of Swetche Systems Limited, reflects precisely the kind of problem-direct experience that distinguishes credible infrastructure builders from opportunistic market participants.

Oyanna’s time at Sterling Bank, one of Nigeria’s established commercial banks, provided direct exposure to the operational realities of correspondent banking: the process of managing nostro accounts, the mechanics of FX conversion, the compliance requirements of international wire transfers, and the friction that institutional processes impose on individual transactions. This experience at the transaction-execution level, rather than at the policy or strategic level, is an unusual foundation for a fintech founder, and it shapes Swetche’s design philosophy in concrete ways.

The procurement and treasury systems expertise that has characterized Oyanna’s subsequent career is equally relevant. Cross-border payment infrastructure is, at its core, a treasury management problem: ensuring that liquidity is available in the right currency, in the right jurisdiction, at the right time, at minimum cost. Founders who approach this challenge from a treasury management perspective, focused on capital efficiency, liquidity optimization, and counterparty risk management, build fundamentally different companies than those who approach it from a pure technology perspective.

Oyanna’s vision of borderless, frictionless financial systems, operationalized through Swetche’s combination of IMTO licensing, multi-currency settlement capability, and stablecoin rail integration, reflects a systemic ambition that extends beyond individual transaction efficiency. The company’s explicit commitment to educating exporters about international payment mechanics, and its advocacy positioning through recognition from peace-focused international organizations, situates Swetche within a broader narrative about the role of financial infrastructure in supporting sustainable, peaceful international economic integration.

This integrated vision, spanning technical infrastructure, regulatory legitimacy, and development advocacy, is characteristic of the most durable infrastructure companies. It reflects an understanding that the long-term success of a payment infrastructure business depends not only on technical execution but on the depth of trust that the company earns from regulators, institutional clients, and the broader communities it serves.

What This Means for Emerging Markets (5 to 10 Year Horizon)

The trajectory of global cross-border payments over the next five to ten years will be shaped by the interaction of several converging forces: the maturation of real-time domestic payment infrastructure in major economies, the regulatory normalization of stablecoin settlement, the expansion of CBDCs, and the continued development of regional payment systems.

The ISO 20022 migration, now substantially complete across major financial markets, will progressively unlock richer data transmission alongside payment messages, enabling more sophisticated reconciliation, compliance screening, and treasury management automation. This improvement in payment data quality will reduce the manual intervention currently required in many cross-border settlement processes and enable more effective straight-through processing.

Central bank digital currencies, currently in various stages of development across more than 130 countries, represent a potentially transformational shift in cross-border settlement architecture over this horizon. Project mBridge, the multi-CBDC platform developed by the BIS Innovation Hub in collaboration with the central banks of China, Hong Kong, Thailand, and the UAE, has demonstrated the technical feasibility of real-time cross-border settlement between participating central banks using digital currencies. If adopted at scale, multi-CBDC platforms could effectively create a parallel settlement layer for interbank cross-border transactions that is independent of the correspondent banking system.

For regulated stablecoin operators, the trajectory of the next five to ten years is likely to be characterized by increasing regulatory formalization across major jurisdictions. The EU’s MiCA framework, the UK’s emerging stablecoin regulatory regime, and the ongoing Congressional deliberations in the United States are converging toward a set of internationally coherent standards for regulated stablecoin issuance and operation.

Africa-specific payment infrastructure developments will be particularly consequential for companies like Swetche. The scaling of PAPSS, the continued development of mobile money interoperability frameworks across the continent, and the gradual improvement of domestic banking infrastructure in major Nigerian, Ghanaian, and East African markets will transform the operating environment for cross-border payment providers serving African corridors. The companies that have invested in regulatory legitimacy and institutional relationships ahead of this infrastructure build-out will be best positioned to capture the resulting growth in formal financial flows.

Read: Why $297 Billion in Q1 Startup Funding Masks the Most Unequal Tech Investment Market in History

Strategic Implications for Investors and Institutions

For institutional investors, the cross-border payment infrastructure segment presents a distinctive risk-return profile relative to consumer fintech. Infrastructure companies benefit from higher switching costs, as institutional clients with integrated treasury and settlement operations rarely change providers without significant operational disruption, along with more predictable revenue streams driven by transaction volume rather than user acquisition. At the same time, the capital intensity of multi-jurisdictional regulatory compliance and the competitive dynamics of a market in which scale advantages are significant create real challenges for smaller operators.

The most compelling investment thesis in cross-border payment infrastructure centers on the combination of regulatory legitimacy and technical architecture. Companies that have invested in building genuine multi-jurisdictional regulatory standing, including IMTO licenses, MSB registrations, and Bureau de Change authorizations that represent years of compliance investment, possess an asset that cannot be quickly replicated by well-capitalized entrants. This regulatory moat is particularly durable in markets like Nigeria, where the CBN’s licensing process is rigorous and the number of licensed IMTO operators remains limited.

For financial institutions including banks, payment processors, and corporate treasury operations, the strategic implication is one of ecosystem engagement. The build-versus-buy calculus for cross-border payment capability is increasingly resolving in favor of partnership with specialized infrastructure providers. The cost of maintaining the full spectrum of correspondent banking relationships, regulatory licenses, and technology infrastructure required for competitive cross-border settlement is prohibitive for all but the largest global banks.

Read: Africa’s Fintech Giants Are Already Regional — But Regulation Isn’t

The Future of Borderless Finance

The transformation of global cross-border payments is not a technology story, though technology is its enabling condition. It is, more fundamentally, a story about the gradual realization of financial fungibility: the progressive elimination of the friction that imposes real economic costs on every transaction that crosses a jurisdictional boundary.

The companies driving this transformation, infrastructure providers like Swetche Systems Limited, are distinguished not by the consumer applications they offer but by the regulatory legitimacy they have earned, the settlement architecture they have built, and the depth of understanding they have developed about the operational realities of international money movement. They are, in the most precise sense, financial infrastructure companies: the plumbing of the global economy.

The significance of this work extends beyond business returns. Efficient cross-border payment infrastructure is a prerequisite for the deeper integration of emerging market economies into the global trading system. It is a determinant of the real income that migrant workers can deliver to families in home countries. It is a condition for the competitiveness of exporters in developing economies seeking to compete in global markets. And it is, in the broadest sense, a dimension of the economic conditions that support stable, peaceful international relationships.

Lucky Koiza Oyanna’s recognition by peace advocacy organizations is not peripheral to his work building Swetche Systems Limited. It is expressive of the same conviction that animates both. The movement of money across borders is, ultimately, an act of economic trust between parties separated by distance, jurisdiction, and often by cultural and political difference. Infrastructure that makes this movement more reliable, more transparent, and more affordable strengthens the economic foundations of that trust.

The future of borderless finance will be built, incrementally, by companies with the technical capability to construct the rails, the regulatory discipline to earn the licenses, and the strategic vision to understand that payment infrastructure is not merely commerce. It is connection.

About the Founder

About the Founder

Lucky Koiza Oyanna is the Founder of Swetche Systems Limited, a cross-border payments and treasury infrastructure company operating across multiple jurisdictions. He focuses on building financial systems that improve global money movement, liquidity management, and interoperability across traditional and digital financial networks.

© 2026 TechChora Global Research. This analysis is prepared for informational purposes and represents the views of the research team based on publicly available information. It does not constitute investment advice. All regulatory frameworks referenced reflect conditions as of the publication date.